Life insurance is one insurance type that, while extremely important, might make many people uncomfortable. No one wants to think about the end of their life, but it’s essential to think about how your dependents will provide for themselves should something happen to you.

A life insurance policy can help your family take care of your final expenses, mortgages, lost income, educational costs, and more after your death. Essentially, life insurance acts as income replacement. When you purchase a life insurance policy, you pay a premium to an insurance company in exchange for the agreement that they will pay out a death benefit to your chosen beneficiaries should you pass away.

Most people, whether or not they realize it, should consider taking out a life insurance policy. There are many different types of life insurance to consider — the two we will focus on in this post are term and whole life insurance.

Term vs whole life insurance: what’s the main difference?

Term life insurance

Term life insurance is a type of insurance policy that provides coverage for a specific amount of time; in most cases somewhere from one to 30 years. When you purchase a term life insurance policy, if you pass away during the covered period of time, the insurance company then pays a death benefit to whomever you have named as the beneficiaries of your policy. However, if you are still alive once the policy ends, your insurance company does not pay out anything at all, and your coverage stops.

Whole life insurance

Whole life insurance, the second type we’ll talk about in this post, is a bit more complicated than term life policies. Whole life insurance is permanent life insurance that both pays out a death benefit and builds up a cash value over time. This means that a portion of each premium payment you make is channeled into a savings component of your policy, called its “cash value”. In some situations, depending on your company and policy, you can choose to withdraw from these funds, or borrow against the amount. Whole life insurance is the most common type of life insurance, and, with this type of policy, you are covered for your entire life, as long as you pay your premiums on time.

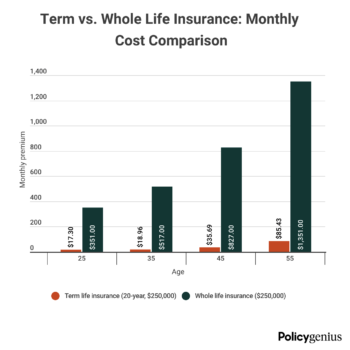

In short, the main difference between these two types of life insurance is the period of time covered. Term life insurance only covers you for a certain period of time, whereas whole life insurance covers you throughout your entire life. Whole life insurance is also a bit more complicated of a product and includes an investment account.

Term life insurance

Now that we’ve got the very basic definitions and differences down pat, let’s dive into term life insurance in greater detail.

For many people in a variety of circumstances, the limited nature of term life insurance makes it the ideal form of coverage. With term life insurance, you can accurately predict what your payments will be on a monthly basis. What’s more, this form of coverage might be appealing if you want to avoid being locked into payments over the long term, if you’re worried they might become unaffordable in the long term.

While we mentioned above that, if you are still alive and well at the end of the specified term of your term life insurance policy, your policy simply ends, in some cases your policy may be convertible. This means that, though you may have to make higher monthly payments, you may be able to renew your term life insurance policy or purchase a new one.

Something else worth noting about term life insurance policies is that they can be classified into two subcategories: level and decreasing.

- Level term life insurance: Level term life insurance policies are the more common of the two types of term life insurances. In these types of policies, the death benefit never decreases. In other words, the dollar amount of the benefit stays level.

- Decreasing term life insurance: With this type of policy, the amount of your death benefit payout decreases over your term. Since your coverage amount decreases over time, your premium will likely be lower than with many other types of policies.

Pros and cons of term life insurance

Even if you’re fairly certain term life insurance might be the right choice for you, it’s worth slowing down to consider the pros and cons.

Pros

- Can potentially be converted to whole life insurance at the end of your term

- Your beneficiaries will receive a larger payout if you should pass away during your covered term

- Premiums are generally more affordable

Cons

- Your coverage is temporary

- It can be more difficult to qualify for this type of plan if you have any significant health issue

- This type of policy doesn’t accumulate any cash value

- Your premiums can go up if you take out a new term

- You must requalify at the end of your term

Whole life insurance

Whole life insurance is by far the most common type of permanent life insurance. It offers you coverage for the entirety of your life, as well as an investment component called a cash-value account.

Because your whole life policy increases in value over time, you may be able to take out a loan against the policy or use it as a source of emergency funds should you ever need one.

The cost of a whole life insurance policy varies depending upon various factors, such as how much coverage you choose to buy and what company you buy through. Your health, age, and gender also come into play. You may also have different options regarding how often you pay your premiums. However, paying monthly, quarterly, or twice a year, rather than just once per year, might incur additional fees.

Finally, while it’s worth noting that your whole life insurance premiums are not tax deductible for you, your beneficiaries would likely not have to pay taxes on the death benefit they receive upon your passing.

Pros and cons of whole life insurance

Because whole life insurance offers fixed premiums and death benefit guarantees, whole life insurance might be a good fit for people who prefer predictability over time. If this is you, read through the pros and cons of this type of insurance to make sure you’re making the best decision.

Pros

- Permanency of your policy

- Predictable payments

- Tax breaks for your beneficiaries

- Potential to use your policy as loan collateral

Cons

- Higher cost than term life plans

- Your beneficiaries receive a smaller death benefit

- Lack of investment control

Which one is right for you?

What type of life insurance policy you need is probably the second most-asked life insurance question, right behind whether you need a life insurance policy in the first place. Different people need different types of insurance; there are no cookie-cutter solutions here. Thinking about the factors below can help you decide whether term or whole life insurance is right for you.

What to consider

Age

Your age can determine which type of policy is right for you, as well as, in some cases, which policies you are even eligible for.

Sex

Currently, cisgender women in the US tend to live about seven years longer than cisgender men. While this gap is shrinking, and the underlying studies neglect trans and gender non-conforming populations, for the moment you must select male or female when applying for a policy, which will affect your overall price.

Health

Most insurance companies will require you to either get a physical or fill out a medical questionnaire before taking out a policy. The healthier you are, the less you can expect to pay.

Budget

Term life insurance tends to be less expensive than whole life policies, as term life policies do not last as long.

Market knowledge

Some permanent and whole life policies can be used to build cash value, which is worth considering if you think you may want to borrow against your account value in the future.

When to choose term life

Term life insurance might be the better choice for you if you are on a budget, only need insurance for a specific length of time, such as to cover a 30-year mortgage, or if your main concern is making sure your family is taken care of, rather than using your policy as an investment.

When to choose whole life

Whole life insurance is the right choice for you if you are interested in building equity, want your insurance to cover you for your entire life, or can afford the higher initial premiums that go along with a whole life policy.

Other life insurance options

A few other life insurance options include:

- Universal life insurance: This is another type of permanent policy that offers a bit more flexibility than whole life policies. Universal policies allow you to increase or decrease your death benefit, and adjust or skip your monthly premium for specific reasons.

- Variable life insurance: A variable life insurance policy consists of a face value death benefit and a cash value that varies with the performance of your investments, making it a riskier type of permanent insurance.

- Final expense life insurance: This permanent policy type is also known as funeral insurance. It offers a smaller death benefit meant to help handle your eventual funeral costs, medical bills, and outstanding credit card debts.

Life insurance will never be an entirely simple topic, but we hope you now have a better understanding of what type of policy is right for you. Visit our life insurance page to learn more, or get a quote today.

Article last updated on March 27th, 2026 at 3:04 pm

The information provided on this page is for informational purposes only and does not constitute an insurance policy or refer to any specific policy. It does not alter or supersede any provisions, limitations, exclusions or conditions expressly outlined in your individual policy documents. For a full description of coverage, please refer to your policy or contact an Elephant Insurance representative.