- Home

- »

- Blog

- »

- Car Insurance

- »

- Does car insurance go down when you turn 25 get a quote

For car insurance providers, age is one of the many factors considered when determining your insurance rate. Why? Your age is often a good indicator of your driving experience and accident risk. When you’ve had more time and practice behind the wheel, you’re much less likely to get into an accident—meaning you’ll cost your insurance provider less to insure and they can charge you a lower premium price.

However, there’s a certain misconception floating around that twenty-five is the magic age you have to wait for to see your car insurance rates drop. While you most likely will be paying significantly less than when you were a teenager, you may not see a huge price reduction on your twenty-fifth birthday. That’s because:

- Your age alone doesn’t determine your premium rate or override other important factors.

- You’ll actually see a pretty steady decrease in rates throughout your teens as opposed to an overnight dramatic drop.

Let’s look at how age affects your insurance, why younger drivers pay higher premiums, and how they can save on their insurance despite their age.

Why are premiums so expensive for young drivers?

Like we mentioned, in insurance provider’s eyes, young drivers are more likely to get into an accident than older drivers, which makes them riskier to insure. According to The Insurance Institute for Highway Safety (IIHS):

- In the United States, the fatal crash rate per mile driven for sixteen to nineteen-year-olds is nearly three times the rate for drivers ages twenty and over.

- Based on police-reported crashes of all severities, the crash rate for sixteen–nineteen-year-olds is nearly four times the rate for drivers twenty and older.

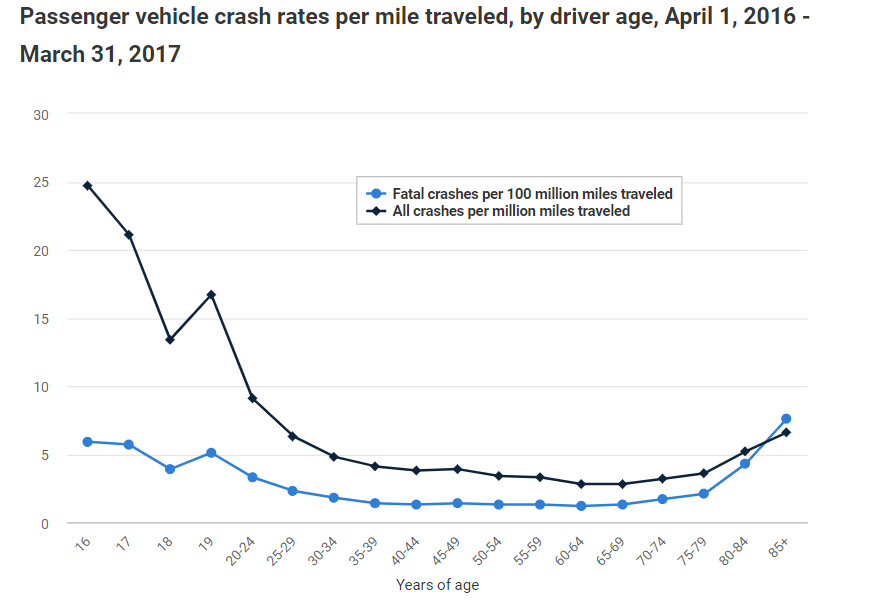

To further illustrate, the IIHS created the following graphic on crash rates by age in recent years:

Just look at the sharp plummet in accidents between ages sixteen and eighteen, then again from nineteen to twenty! From then on, crashes seem to level out regardless of age, then creep back up as drivers reach their late seventies and early eighties.

At what ages do car insurance rates go down?

So, does that mean elderly drivers usually see higher premium rates, just like young drivers? Sure does! But let’s take a step back.

In general, the older you get, the less expensive your insurance will be — up to a certain point. Like we mentioned, teens and young adults are seen as one of the riskiest age groups to insure due to their lack of experience behind the wheel. But what about that magic age of twenty-five? Does your car insurance rate plummet the date of your quarter-life birthday? Not so much.

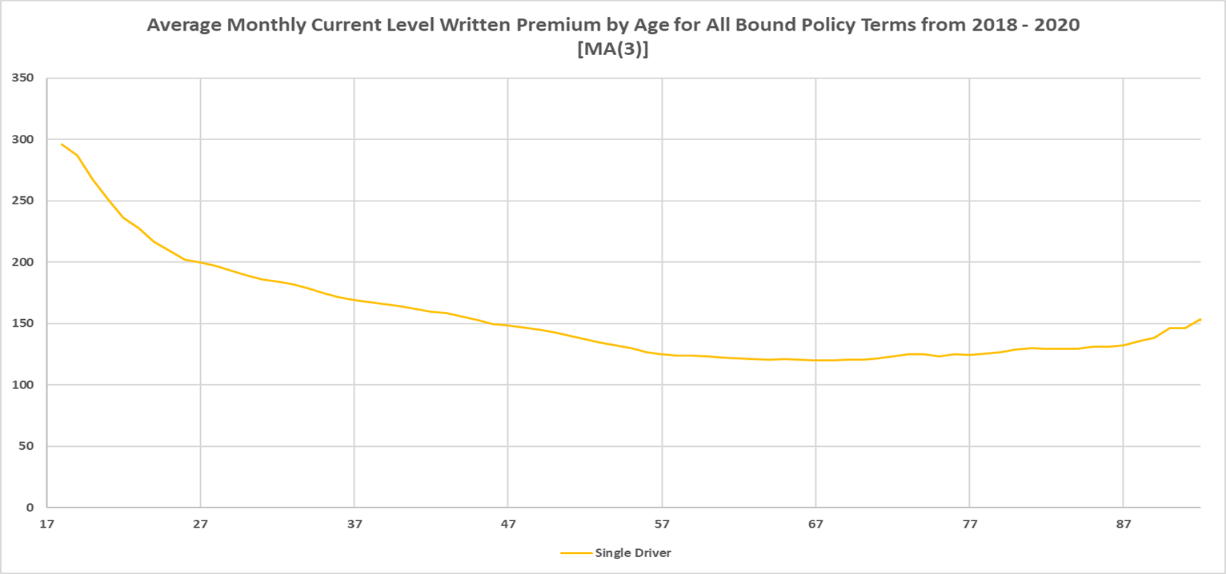

According to our analysis, once most drivers turn twenty-five, they’ve already seen the biggest drops in their insurance premium — in their teens and early twenties. Their premiums do often go down at twenty-five, but not dramatically (or magically!) from age twenty-four. Check out our graph that shows the average monthly premium cost by age in Elephant’s most recent underwriting years:

Our data suggests that there are few ages that see a singularly huge drop. In general, your insurance rate will dwindle a little more each year. The steepest drop actually seems to occur between our drivers’ eighteenth birthdays and twenty-first birthdays, where they go from paying an average of $1,842 for their six month polices to only $1,488 (a nineteen percent decrease). After turning twenty-one, drivers usually continue to see their rates drop each birthday, but the difference each year becomes smaller and smaller.

Now back to our elderly drivers group. As you can see, once drivers start hitting their mid-seventies, their insurance rates start creeping back up again. Unfortunately, the older we get, the worse our reaction times and reflexes become, which makes us more dangerous behind the wheel — and riskier for insurance companies to insure.

Does gender play a role?

Unless you live in a state that has outlawed insurance rate variances by gender, gender will play a role in your rate. Men on average, especially young men, pay more for car insurance than women. That’s largely because statistically, younger men are more likely to:

- Spend more time behind the wheel

- Be involved in a serious accident

- Incur traffic violations

- Engage in drunk driving

- Own cars that are considered higher risk, like sports cars

If you’re a guy reading this and thinking “Hey! I’m really careful, none of those apply to me,” consider asking your insurance provider if they offer car tracking devices to monitor your driving habits. If they do, you might be able to reduce your premium despite being a young male driver.

The gap between what young men and women will spend on car insurance is most dramatic in their earlier years, usually between the ages of sixteen–twenty-three. Once they start hitting twenty-three–twenty-four, most will notice a fairly dramatic drop in price. Going forward, between twenty-four and twenty-five, it starts leveling out, but men may actually continue to see drops in price until they’re about thirty-two.

Why might insurance rates not fall for a driver at 25?

Insurance rates are tied to risk, so even if you’re in your mid-twenties, your driving record may keep your insurance rates higher. Have you racked up a number of traffic tickets? Have you had several accidents? If so, your risk profile will remain high, regardless of your age. Other risky behaviors or incidents that will cause your rate to stay high are things like a DUI ticket or having a low credit score. Another reason might be if you start driving for a ride-sharing service; your insurance rate my stay high since commercial drivers face additional risks.

How can younger drivers reduce their insurance rates?

Savings for students

Student Away at School Discount

If you’re still a college student going to school away from home, and you’re only using your car when you’re visiting home, why pay a higher monthly rate on a car you’re barely using? Ask your provider if you qualify for a Student Away at School discount.

Good Student Discount

Good grades may equal a better auto insurance rate for students. Many insurance providers use good report cards as a rough proxy for a credit score to determine responsibility, since teenagers are less likely to have had time to build up a good score.

A Good Student Discount can help young drivers lower their premiums if they have an A or B average. The size of the good student discount will depend on your insurer. Student drivers hoping to qualify for the discount will usually be asked to submit their report card once or twice a year to prove they’re maintaining good grades. What’s more, this discount can last you from high school through college!

Multi-Car Discount

If you’re still on a shared insurance policy, like with your parents, a Multi-Car Discount usually leads to lower premiums for everyone on the policy. It’s often one of the largest discounts you can qualify for on an insurance plan!

Higher Deductible

Insurance premiums are based on the odds that your insurance company will have to pay out on a claim (and the estimated size of the claim). Raising your deductible means you’re willing to pay more out-of-pocket in the event of damages to or loss of your car before your insurance kicks in. If you’re willing to shoulder a little more cost up front, your insurance provider will charge you less each month for the cost of your insurance premium. A good way to think of it is sort of like paying a down payment on a house. The more you pay up front, the lower your monthly mortgage payments will be.

Raise Your Comprehensive and Collision Coverages

Comprehensive and Collision insurance covers far more than what a mandatory minimum auto insurance policy would. For example, Comprehensive covers damage from things like theft, flood, tree branches falling on your car. Collision covers damage to your car when you collide with another vehicle or object, like a car, pole, or another non-living object. And, since we’ve just learned that younger drivers are more likely to be in an accident, we feel confident encouraging all young drivers to have both these coverages on their policies. Otherwise, they may be on the hook for large out-of-pocket expenses if they find themselves in an accident.

There are so many ways drivers of all ages can lower their premiums with the right insurance provider. See your options in a way that makes sense (and what discounts you might qualify for) when you get a quote with Elephant.

This article is intended for informational purposes only. It does not replace or modify the information contained in your insurance policy and may not reflect the official policies of Elephant Insurance or current developments.

Article last updated on June 19th, 2026 at 2:06 pm

The information provided on this page is for informational purposes only and does not constitute an insurance policy or refer to any specific policy. It does not alter or supersede any provisions, limitations, exclusions or conditions expressly outlined in your individual policy documents. For a full description of coverage, please refer to your policy or contact an Elephant Insurance representative.